What You Need to Know About Reverse Mortgages: An In-Depth Look at Reverse Mortgages

A reverse mortgage is a helpful financial product that allows homeowners aged 62 and older to convert part of the equity in their homes into untaxed funds. This product allows individuals to access the wealth they have built in their homes without the need to sell their property or take on new monthly payments. But how exactly does a reverse mortgage work? In this article, we will explore the details of reverse mortgages and how they can aid homeowners who want to boost their retirement income.

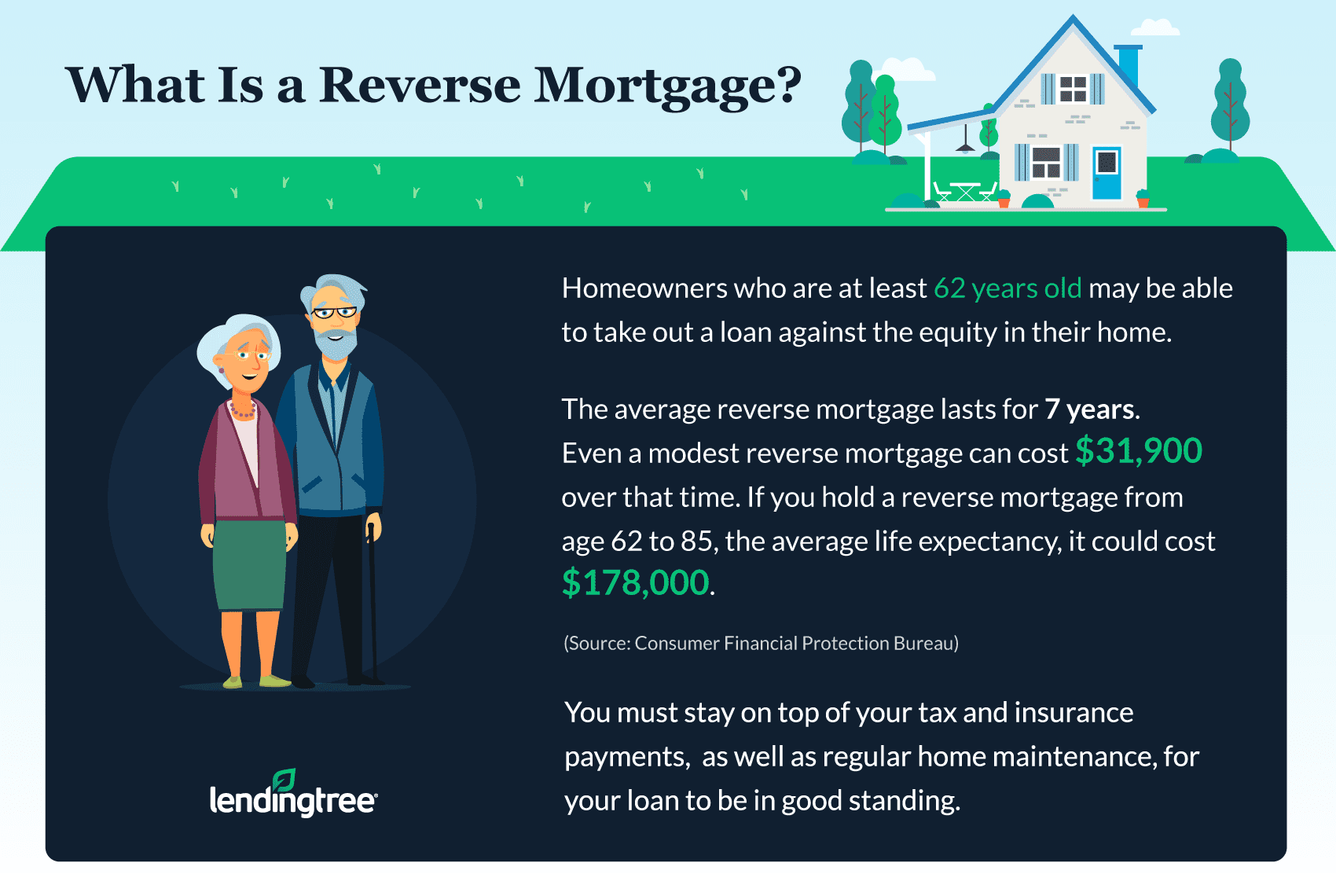

What Is a Reverse Mortgage?

A reverse mortgage is a loan designed for older homeowners that lets them borrow against the equity they have built up in their home. Unlike traditional mortgages, individuals are not required to make monthly payments. Instead, the loan is repaid when the homeowner sells the home, moves out, or passes away. Reverse mortgage loan is determined based on factors such as the value of the home, the homeowner's age, and the current interest rate.

How Does a Reverse Mortgage Work?

In a reverse mortgage, borrowers can receive funds in several ways: a lump sum, monthly payments, or a line of credit. The funds received can be used for any purpose, from paying bills to funding healthcare costs, or simply enhancing their retirement lifestyle. The loan repayment happens after the homeowner no longer resides in the home, either by selling the property or passing away. The equity in the home typically covers the loan, and any remaining equity is passed on to the homeowner's heirs.

Pros and Cons of Reverse Mortgages

As with any financial product, reverse mortgages come with both benefits and drawbacks. Below, we’ll examine some of the pros and potential risks of reverse mortgages:

- Pros:

- Provides additional retirement income without monthly payments.

- Seniors can stay in their homes for as long as they live or until they move out.

- No required payments are necessary.

- Cons:

- Interest charges can be higher than traditional mortgages.

- May decrease the equity in the home, leaving less for heirs.

- Fees and closing costs can be substantial.

Eligibility for a Reverse Mortgage

To qualify for a reverse mortgage, there are certain requirements that must be met. Some of the basic eligibility criteria include:

- The homeowner must be at least sixty-two years old.

- The home must be their primary residence.

- The homeowner must have sufficient equity in the home.

- The homeowner must be able to pay for ongoing property taxes, insurance, and maintenance costs.

Types of Reverse Mortgages

There are several different types of reverse mortgages available, including:

- Home Equity Conversion Mortgages (HECMs): This is the most common type of reverse mortgage , insured by the federal government.

- Proprietary Reverse Mortgages: These are private loans not backed by the government.

- Single-Purpose Reverse Mortgages: These are typically offered by state and local governments for specific purposes, such as home repairs.

Each type of reverse mortgage has its own benefits and requirements, so it’s important to carefully consider which one is best for your needs.

Frequently Asked Questions (FAQs) About Reverse Mortgages

- What is the main advantage of a reverse mortgage? One of the top reasons for a reverse mortgage is that it provides seniors with access to home equity without requiring monthly payments.

- Can I still own my home with a reverse mortgage? Yes, with a reverse mortgage, you retain ownership of your home. You can stay in the home until you move or pass away.

- Do I have to pay back a reverse mortgage? The loan is repaid when you sell the home, move out, or pass away. The proceeds from the sale of the home will usually cover the loan balance.

- Are there fees associated with reverse mortgages? Yes, there are fees, including origination fees, closing costs, and servicing fees. These costs can add up.